After accepting the binding offer and signing the purchase agreement you are not yet done. Depending how the deal is structured you might need to perform substantial work and even the purchase price can change.

Whether or not the purchase price can change depends if the deal is structured as a locked box or with completion accounts.

Locked box versus completion accounts

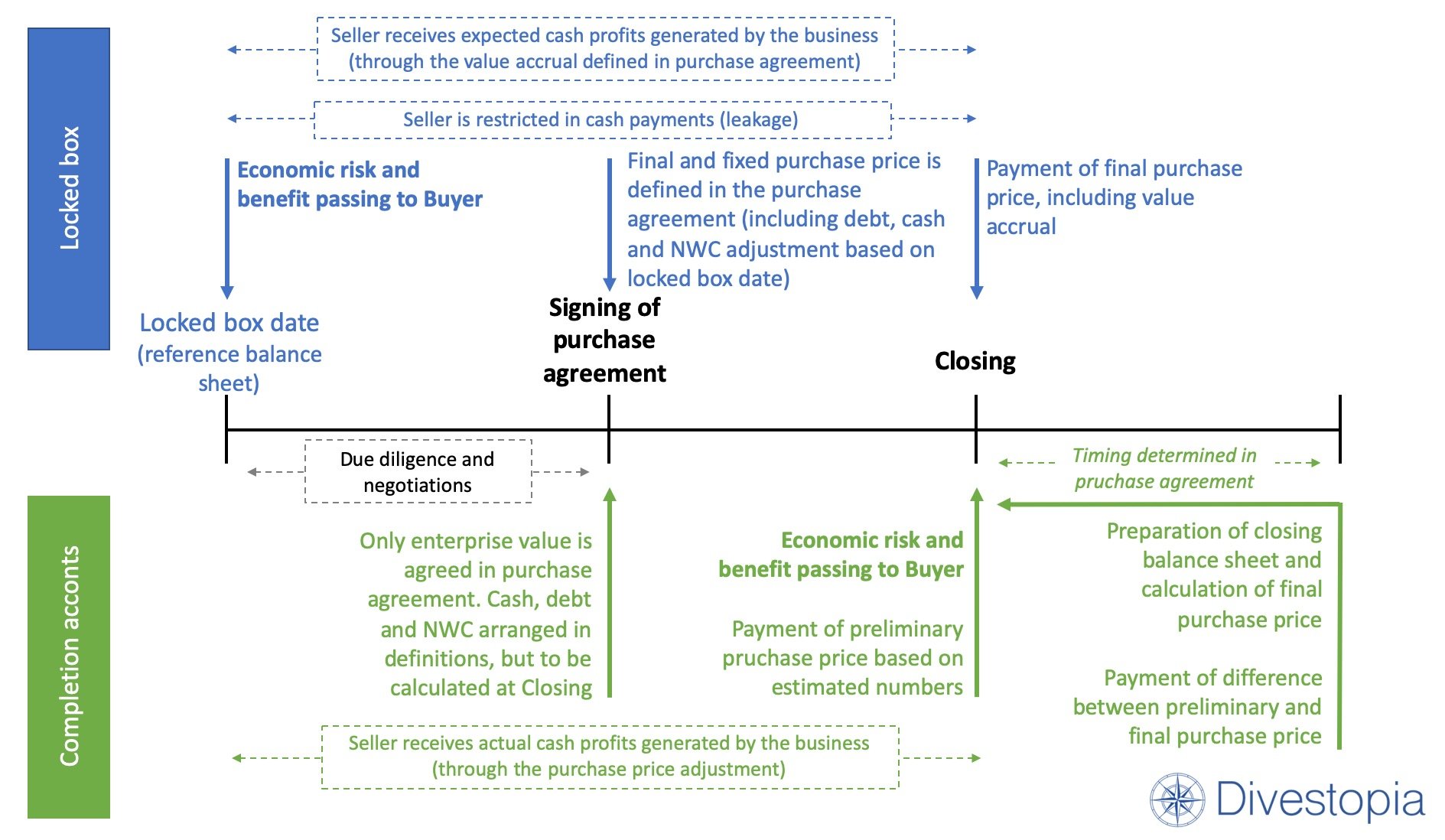

Locked box

In a locked box the enterprise value and equity value are fixed. The date on which the numbers are fixed is called the locked box date, which is often the financial year-end. The Buyer makes its assessment of the enterprise value, the net debt position and the working capital variance adjustment based on that date. The purchase agreement includes the EV to equity bridge as an appendix so that these numbers are fixed.

The period from the locked box date to the Closing date is called the locked box period. The Buyer has legal ownership of your business after Closing. In the locked box period you as an owner receive compensation for running the business. This is a so-called value accrual and calculated as a percentage over the equity value. The percentage presents the net cash earned by the business in the locked box period, but most of the time is based on negotiations between Buyer and Seller. In the locked box period you are limited in cash payouts (so-called leakages). For example, you are not allowed to distribute dividends or perform other non-operational payments to yourself. In the purchase agreement it is important to define which are permitted payments and which are leakages.

Completion accounts

With completion accounts only the enterprise value is fixed. The equity value is determined at Closing. In a completion account process, the Seller prepares an estimated closing balance sheet just before actual closing date. Based on those numbers the estimated equity value and purchase price is calculated. This estimated preliminary purchase price is paid by Buyer to Seller (often at signing of the purchase agreement).

The purchase agreement includes a timeframe within what time the Buyer (which is now the new owner) has to provide the final closing balance sheet. Based on the final closing balance sheet a final equity value (purchase price) is calculated, including final cash, debt and working capital balances. Any differences with the preliminary purchase price paid is either paid (by Buyer) or reimbursed (by Seller).

The purchase agreement should include a detailed description of indebtedness and cash in order to allocate the balance sheet accounts to debt/cash or net working capital. Preferably, the classification is on trial balance account level. For an Excel template of a Closing balance sheet click here.

Main differences

Key differences between locked box and completion accounts:

- In a locked box the equity value is known at signing. The purchase agreement focuses on making sure that no unpermitted payments are done in the locked box period (i.e., leakages).

- As the equity value and final purchase price is not known when using completion accounts, the purchase agreement focuses on definitions of cash, debt and working capital. These definitions need to be as clearly defined as possible to prevent discussion afterwards.

- The purchase price you receive as a Seller is uncertain when using completion accounts. Also, substantial work, including external financials advisors are needed to prepare and review the closing balance sheet. In many cases discussions arise what to consider debt, cash or working capital. The purchase agreement includes a dispute resolution process, including the involvement of an independent accountant, should any unresolved discussions exist.

What is best for your transaction?

A locked box transaction provides more certainty for a Seller, as the purchase price is known at the moment of signing. That is why this is a very common type used in auction processes. However, for using locked box you need to have detailed financials at the locked box date, which potential Buyers can use to determine the enterprise value, cash, debt and the NWC variance adjustment.

The transaction type is very region dependent. Locked box is common in Europe and the UK. In the US, Latin America, Asia and rest of the world completion accounts are generally used. When opting for a transaction type which is not common in your region make sure your advisor is sufficiently knowledgeable about it! Even experienced transaction advisors have difficulty understanding the mechanics when they have never actually done deals using these types. Many deals have failed due to an incorrect use of locked box mechanism.

Common mistakes

Common mistakes and misunderstandings regarding locked box:

- “In a locked box there is no working capital adjustment”. This is wrong. Similar to completion accounts, in locked box there is a net working capital variance adjustment. The difference is that this variance is calculated at the locked box date, using the historical monthly numbers and the locked box date working capital position as the actual position.

- “A Seller can pay-out whatever they want in the lockbox period, such as pay-out dividends”. Again, wrong. It is important to define leakages in the purchase agreement to ensure no cash is taken out in the locked box period. Additionally, a Buyer can perform a leakage review to ensure no unpermitted payments occurred.

- “A Seller can manipulate working capital in the locked box period and not pay its creditors”. While true, there is no incentive for a Seller to do this. Not paying the creditors’ results in more cash, but the equity value is fixed at the locked box date. So, the increased cash position is attributable to the new owner. Also, the purchase agreement includes a clause indicating that the business has to be operated in its normal course of business.

- “A Buyer can do its detailed due diligence after signing”. This is impossible. As the full enterprise to equity value needs to be defined in the purchase agreement it is crucial that Buyers have the opportunity to perform a full due diligence before signing. If the purchase price can change post-signing it is not a locked box.

Find more on:

- Adjusted EBITDA and EV to equity value bridge

- Free M&A Excel templates for download

- Normal level of net working capital at Closing

- Choosing and preparing a virtual data room