The impact of the Corona virus (COVID-19) is large: in order to prevent excessive outbreak of contamination governments are closing borders of their countries, closing bars, restaurants, shops and in some cases quarantining people to their houses. While difficult to foresee, this article will elaborate on the (short-term) impact of the virus on the M&A landscape and how to present deal financials excluding this non-recurring impact. It is written purely from an economic point of view on the M&A market. This article contains excerpts from an article written by Pierre-Olivier Gourinchas (Professor of Economics at UC Berkely).

Impact on the economy

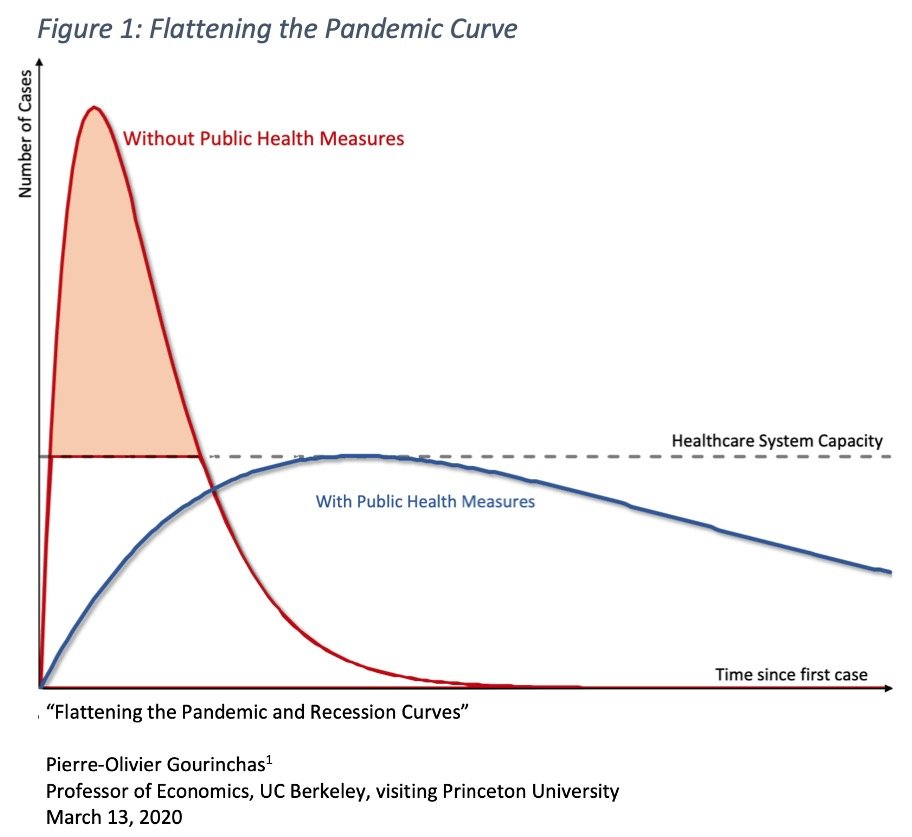

The current – correct – government focus is on containing the pandemic in order to not overwhelm the health system. The health system capacity is limited (e.g., in number of intensive care units, equipment, health professionals). If the number of infected patients which require intensive care help exceeds the maximum level the health system would be overwhelmed with all consequences that entails. The below figure presents the impact (in red) if the number of cases at one moment in time exceed the health care capacity. To not exceed the number of cases the healthcare system can adequately handle, governments are taking measures to “smooth-out” the impact and “flatten the pandemic curve”. These measures are aimed at limiting contact between persons and by doing so reducing the transmission rate of the virus.

While being a solution for trying to contain the pandemic, these measures have a negative impact on the economic activity. The temporary closing of businesses, schools, restaurants, bars and decrease of the working population by staying at home, negatively affects the productivity. The longer this takes, the higher the impact. Additionally, the fear resulting from the pandemic could have a ripple effect: by consumers limiting their spending, which consequently decreases demand (directly visible in the tourism, travel and leisure sector, but indirect impacting other sectors as well). Less demand results in businesses cutting costs in order to survive, likely by reducing salaries (initially reducing temporary workers but if needed fixed employees as well). Failure to cut sufficient costs, results in bankruptcy, which in turn could result in non-payment of bank loans. Increasing non-payment of loans will make banks more hesitant in providing new loans. This overall loss of confidence could start a vicious circle.

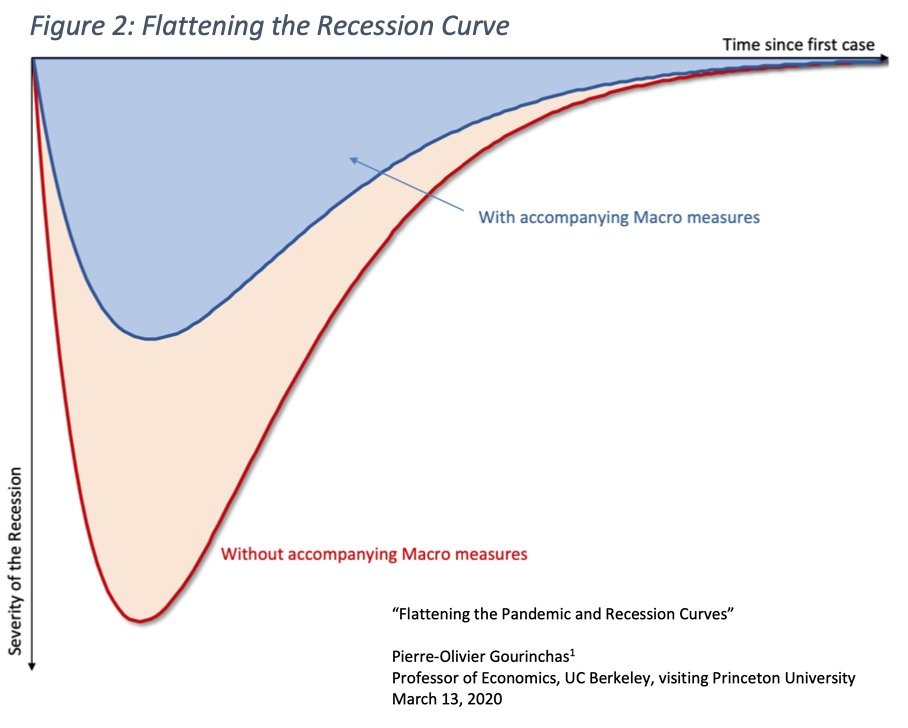

As per Pierre-Olivier Gourinchas governments should take direct action to prevent this vicious circle and reduce impact of the severity of a recession (and make sure the recession curve is “flattened” as per the figure below). Measures governments should take encompass: (i) ensuring that workers remain employed and keep receiving salaries, (ii) easier borrowing terms or other financial support for businesses to limit bankruptcies and (iii) support the financial system, especially regarding non-performing loans. For more details refer to the article.

Impact Corona virus on M&A deals

While the impact on the economy is large, a loss of confidence and increased uncertainty is lethal for M&A deals. This level of uncertainty negatively impacts all M&A activity in the short term. Companies first need to bring their own business in order before looking at acquisitions. Especially, small- and medium sized companies could have insufficient reserves to survive the loss of income and the coming economic downturn. For relatively larger companies this provides opportunities to buy distressed companies against a discount. To understand the impact on ongoing M&A deals a distinction needs to be made between deals ongoing and signed deals.

On-going deals

On-going or upcoming deals include deals where the sales process has started and potential investors have expressed their interest and agreed non-binding offers. Given the uncertainty on the magnitude of the impact the virus will have on businesses, these sales processes will be put on hold. Strengthened by practical limitations such as travel bans which make it impossible to hold face-to-face meetings between Buyer and Seller. As the offers are non-binding there is no legal obligation for a Buyer to continue with the acquisition. New processes or just started sales processes will be postponed.

Signed deals

When there is a signed deal (i.e., there is an agreed and signed purchase agreement) the situation is different. In this situation it is important to know where in the process the deal is. If the deal is already Closed, the legal ownership has passed to the Buyer and the deal cannot be undone. It could be there is an earn out agreed, which is now at risk.

In the period between signing and Closing the clauses in the purchase agreement need to be followed. The applicable clause to consider is the Material Adverse Change (MAC)-clause, also known as the Material Adverse Event (MAE)-clause or “force majeure“.

A Material Adverse Change is often defined broad in a purchase agreement and could be defined as: “MAC” means a material adverse change in the assets, business, operations, liabilities, performance, results of operations or financial condition of the Company.

The goal of a MAC-clause is to protect a Buyer against any circumstance or change which materially impacted the value of the acquired business, which was agreed at the moment of signing the purchase agreement. Of course, the material adverse event should not be foreseen at the moment of singing. In order to limit the exposure, the MAC-clause could be quantified and include certain financial metrics (e.g., sales underperformance of 30% compared to the budget). Buyers could also try to expand the event to the future and include “prospect” in the definition of the MAC. As a Seller this should be avoided.

A MAC-clause is most of the time used as a condition precedent to Closing in the purchase agreement. Meaning, that in the case a material event (following the definition in the purchase agreement) has passed before Closing, the Buyer has the right to cancel the deal and walk away.

Given the uniqueness of the Corona pandemic it is unclear if this follows the broad MAC definition (i.e., lack of prior jurisdiction), but that the business is materially affected is clear. If the MAC-clause is defined more specific and excludes general economic and financial market developments the pandemic will not be a valid reason. However, as most MAC-clauses are defined rather vague this topic could become part of lengthy legal discussion and disputes.

To prevent legal disputes and given the significant implication of the MAC-clause for a Seller, a Buyer can choose not to exercise the clause but to use it to try to lower the purchase price.

Impact on financials and operations

Most governments are slowly reducing the COVID-19 related restrictions and are allowing more businesses to open and (people) movements to occur. While the risk of a second pandemic remains a real possibility, the question is now how the “new” distance economy will look like.

For business owners this crisis had a gigantic impact on the operations, reflected both in the income statement and balance sheet. For business owners thinking to sell their business in a short term it is crucial to think about how to present the impact of this “non-recurring” event on their deal financials.

Income statement

The value of a business is derived from its free cash flows. The valuation of a business on the future free cash flows. The last year realized free cash flow is used as a starting point for the future years. But what happens if the last year free cash flow is not representative for the future years? For example, in the case of a worldwide virus outbreak.

In any upcoming deal the impact of the pandemic on the business needs to be clearly described, both in quantitative terms and qualitative terms. What was the impact of the huge drop in both demand and supply? Did the business close or were its customers and supply lines not impacted? For any upcoming deals the following needs to be described in detail, most likely in the Information Memorandum:

- When did the Company start to see impact as result of the government measures to control the COVID-19 outbreak?

- How did the decrease in supply and demand impact the business?

- What measures were taken by the Company to prevent further negative impact? For example, closure of factory, firing or special furlough of employees.

- What support was received from the government? In some countries the governments provide support in terms of subsidies, guarantees for loans or (partial) payment of costs. Is this support unconditional or is there a risk of repayment?

- What is the impact on the customer base? Any customers gone bankrupt? What are the legal conditions of a sale, when is ownership of the sold goods transferred and can they be returned?

- What is the impact on the suppliers? How is the supply chain impacted? Both in terms of delivery availabilities (e.g., key suppliers gone bankrupt) and time.

- What agreements were reached with the financing banks? Did they provide a waiver of convenants and accepted a delay in payment of principal and interest?

- Is there an impact on other stakeholders?

Normalize the earnings

The resulting financial impact on the earnings should be normalized as it does not represent a normal recurring event. This is applicable for both negative impacts as well as positive (webshops and supermarkets which saw a huge increase in their revenues).

The best way to normalize the impact is to present weekly financials and extrapolate the earnings from just before the pandemic outbreak. For example, calculate the average revenues and costs per week in January and February, and extrapolate this amount for March to May. Keep track of any seasonality that needs to be adjusted!

Assessing the “one-off” impact on the earnings is complex as the future remains uncertain. If the economy enters a recession it is unlikely the earnings will be the same as before. As such, most Buyers will not (fully) accept extrapolated historical results and will expect a lower purchase price for the increased risk they are running.

A more acceptable way to extrapolate earnings is to extrapolate backwards. Meaning, using the average realized run-rate earnings after the pandemic to extrapolate to the months before. However, for this the Company needs to be realizing sufficient profitable results.

Balance sheet and net working capital

The main impact will be on the earnings. However, the balance sheet impact should not be neglected as it can have a huge impact on a deal. The main impact will be on the net debt position and the normal level of working capital.

To determine the net debt impact a Company needs to assess its short term and non-operational cash outflows as result of the COVID-19 measures. For example, a restructuring provision or a liability for the risk of repayment of government support are considered debt-like.

The net working capital levels are likely impacted as well. It could be the Company agreed special payment terms with its customers or suppliers, resulting in increased trade receivables and trade payables. Inventories can increase due to less sales. Taxes payables can increase in the case of government support for extending payment terms. With these cases setting a “normal” working capital level to be used in the transaction can be difficult. Using a last twelve months as average might not be suitable. A better option is to use a longer term (e.g., 24-months) to set a normal level.

A Buyer will want to be sure that the increased working capital levels are worth paying more for. In the case of increased receivables a guarantee needs to be provided these can be collected and in the case of inventories whether these still can be sold or if they should be considered as obsolete.

Find more on:

- Adjusted EBITDA and EV to equity value bridge

- Free M&A Excel templates for download

- Normal level of net working capital at Closing

- Locked box versus completion accounts

- Choosing and preparing a virtual data room