Next to reference to a cash- and debt-free basis, a received offer will include a statement that a normal level of net working capital needs to be present in the business at Closing. The reason for this is that a new owner on day 1 after acquisition does not want to do a capital injection to fund any working capital needs.

Net working capital definition

Net working capital is defined as the capital of a business which is used in its day-to-day trading operations, calculated as the current assets minus the current liabilities. If this amount is positive it generally means that the business is healthy and can fund future operations and growth.

A high positive working capital amount which is increasing can indicate problems at a business. For example, customers are no longer paying and cause receivables to increase, or sales are down and there are increasing inventories as a result.

Working capital days

As working capital balances and amounts do not mean anything by themselves, the working capital development is always analyzed as a percentage of revenues or by using the following days metrics.

Days Sales Outstanding (DSO): meaning the average days it takes to collect your outstanding receivables. Calculated with the following formula:

[ Accounts receivable / (1 + VAT%) ] / revenues * number of days

Days Payables Outstanding (DPO): meaning the average days after which you pay your payables. Note, payroll costs are excluded as these do not flow over your accounts payable balance as they are paid directly. Calculated with the following formula:

[ Accounts payable / (1 + VAT%) ] / (cost of sales + operating expenses – payroll costs) * number of days

Days Inventory Outstanding (DIO): meaning how it takes before your inventories are sold. Calculated with the following formula:

[ Inventory / cost of sales ] * number of days

Cash Conversion Cycle (CCC): the average total number of days it takes to convert your inventories into cash. Calculated with the following formula:

DSO + DIO – DPO

Net working capital in M&A deals

In a transaction, the concept of working capital is a bit different. While still calculated as current assets minus current liabilities, all cash or debt balances are excluded (as well as any cash-like or debt-like items). Furthermore, working capital is broken down in trade working capital and other working capital.

Trade working capital includes the main accounts needed for the business operations, mostly being inventories, trade receivables and trade payables.

Other working capital includes the remainder of the working capital accounts, such as personnel liabilities, taxes payables and other current payables and receivables.

As the working capital is used to finance the day-to-day operations of the business, for a Buyer it is important they receive a business after acquisition with sufficient working capital. The level of sufficient working capital is defined as the normal level of net working capital.

The normal level of working capital can be explained by buying a car. When buying a car you do not want the tank to be completely empty and you want the car having enough gasoline to at least drive to your home. The car salesman will say that a completely full tank of gasoline is not needed for that either. The average of the tank is seen as a “normal” level of gasoline needed to sell the car.

For a transaction it does not matter if the working capital is positive or negative. As long as it reflects the normal level needed to operate the business and there is no need for an additional capital contribution. For example, a normal negative level of working capital could be applicable in case of direct cash sales (i.e., shops or supermarkets) or business with a high level of prepayments.

Analyzing net working capital

Click here for a net working capital Excel template, including above analysis.

Seasonality

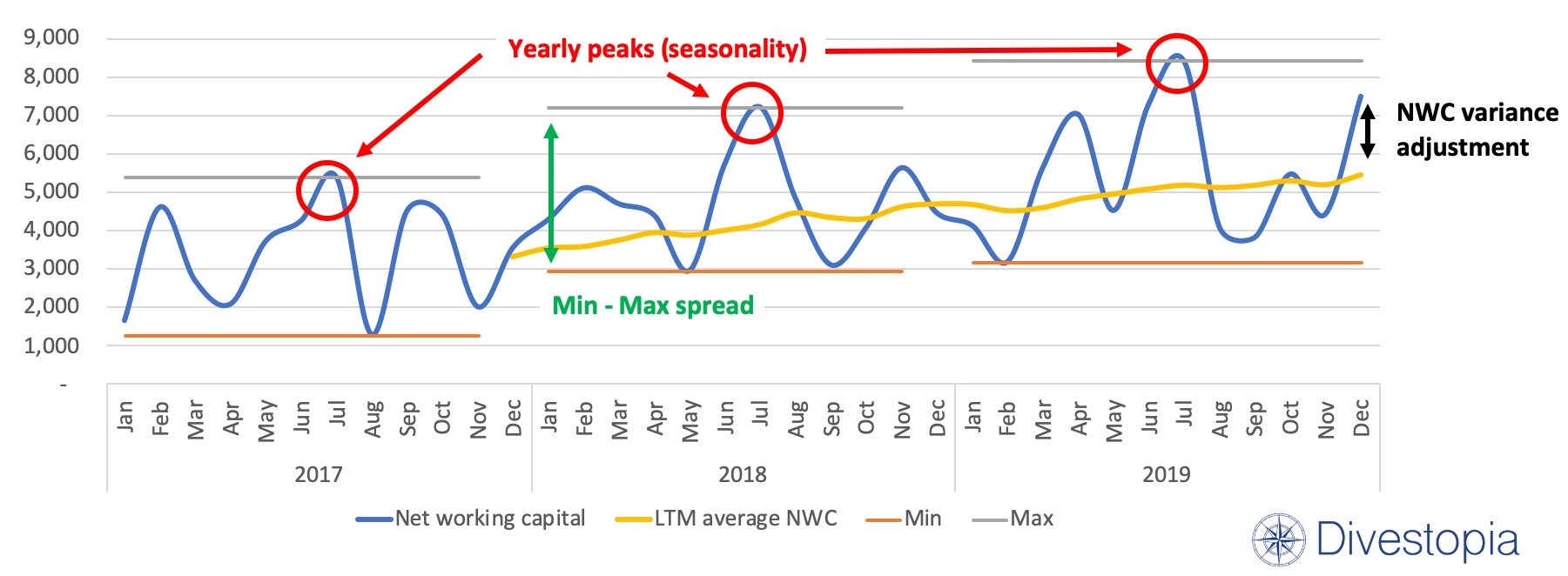

Seasonality in net working capital is important to understand, because that indicates the maximum and minimum financing need in a recurring yearly pattern. In the above graph there is a yearly recurring peak in July. This indicates that the business being analyzed most likely has its sales peak in August to October and needs to build-up inventories in the months before to be able to sell in the months after. In other words, the business needs to invest cash in those months to be able to have sufficient inventory. The cash collection of the sales comes in the months after. The business will need to have an adequate financing arrangement with its bank to support this pattern.

Normal level of net working capital

The normal level of working capital is an amount defined in the purchase agreement and referred to as a net working capital target, a net working capital peg or net working capital true up. The required level of working capital is generally calculated as the average of the last twelve months (LTM). By taking twelve months any seasonality impact is included. In some situations another metric might be more suitable. For example, in a fast growing business or in a high-inflationary environment. A last 3 or last 6 months average might be more adequate in those situations.

A Seller always wants to set the normal level of required working capital as low as possible, whereas a Buyer wants to set it as high as possible.

Net working capital variance adjustment

If your level of working capital is not at the normal level at Closing this is adjusted in the purchase price. This adjustment can either be an addition to the purchase price (when the actual working capital at Closing is higher than the normal level) or a deduction (when actual working capital is lower than normal at Closing).

In the above graph the actual NWC is higher than the NWC average of the last twelve months (LTM), meaning that if the Closing occurs on this date there will be an addition to the purchase price.

Timing of a sale and impact of net working capital

The timing of a sale should not materially impact the purchase price of a business. If the sale is taking place later only the net cash realized in that time period should be added to the purchase price. Another reason for including a net working capital adjustment as part of the purchase price is to ensure no material deviations occur in the price depending on the timing.

For example, looking at above graph, if there is no NWC adjustment included in the purchase price and the Closing takes places in July, the Seller will point out he is missing money because he just financed the build-up of the working capital levels. The Buyer will profit from that in the months after when sales take place and money is collected. If the sale of the business takes place in August, the Buyer will state he needs to finance a complete build-up of working capital and loses money.

With a NWC variance adjustment this impact is neutralized:

– If the sale occurs in July, the Seller receives a plus on the purchase price because of a higher working capital level than normal required, but the cash level will be lower as result of this build-up.

– If the sale occurs in August, the purchase price needs to be lower as the actual level of NWC is lower than the normal level, but the Seller will receive more cash as part of the Equity value due to collection of sales.

A good net working capital variance adjustment protects both a Buyer and a Seller

Find more on:

- Adjusted EBITDA and EV to equity value bridge

- Free M&A Excel templates for download

- Locked box versus completion accounts

- Choosing and preparing a virtual data room